Brian Pearce, IATA’s chief economist, admits: “It feels like quite a challenging environment at the moment because we’ve had very sharply rising oil and jet fuel prices. Jet fuel is up nearly 50% on where it was this time last year and we’re seeing all sorts of geopolitical risks, not least the tariff war that’s broken out on steel and aluminium.

“We’re facing the headwinds of rising costs - so far, airlines have been able to keep up with that through better unit revenues, partly through higher load factors and slightly firmer pricing as well. But this latest acceleration in fuel costs is going to be quite a challenge for the industry to overcome.”

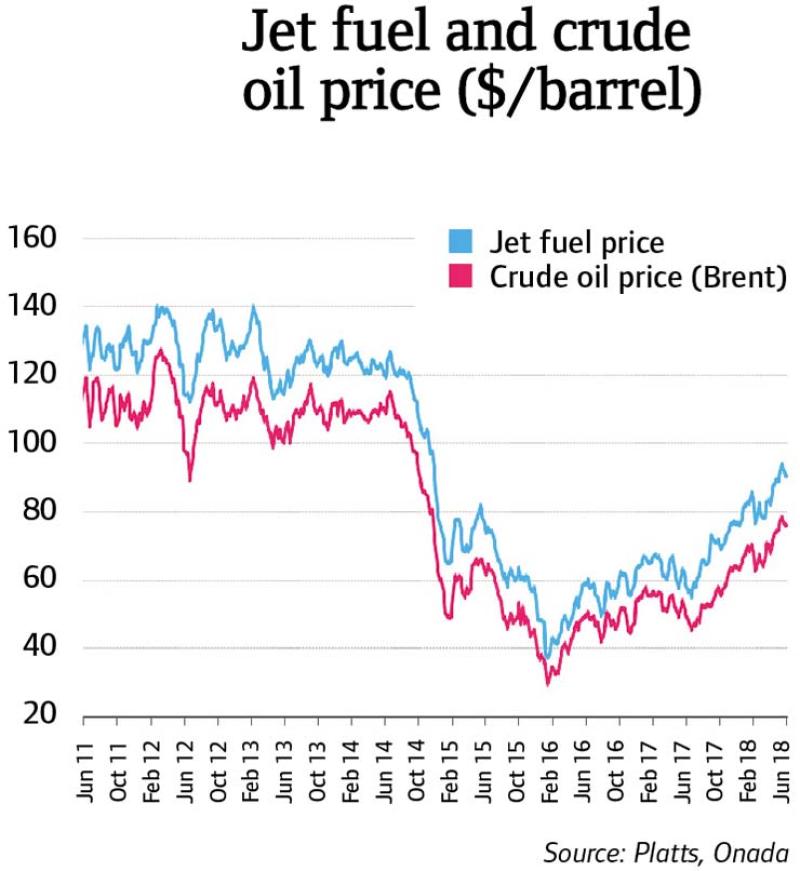

The industry has, of course, been here before and the price of oil is not currently undergoing the kind of volatility endured in 2008, when prices swung wildly between $40 and $147 per barrel, with an overall average price of $99.

It should also be remembered that the price of jet fuel in 2018 is only back to the levels last seen in late 2015 before the oil-price crash that meant a barrel of jet fuel dipped to below $40 per barrel in early 2016.

Hedging their bets

How quickly airlines will be affected by this hike in fuel prices will depend on their own individual circumstances and particularly any fuel hedges they have in place.

For example, European carriers have generally continued to hedge a higher proportion of their fuel bills in recent years, despite low oil prices. Meanwhile, North American carriers – particularly the big three US airlines (Delta Air Lines, American Airlines and United Airlines) – have largely avoided fuel hedging in recent years. This means that any impact of the higher fuel costs is likely to be felt much more quickly in North America than in Europe, although the situation will vary by carrier.

Ryanair’s CEO Michael O’Leary says the low-cost carrier has hedged around 90% of its fuel requirements up to March 2019 at around $58 per barrel. But he still expects fuel to be “a major cost headwind for the next 24 months”.

“A lot depends on what happens to the price of oil – we’re well hedged for the next 12 months,” adds O’Leary. “There tends to be a 12-month lag between fuel and airfares.

“With spot prices at $80 per barrel, I think that’s going to lead to a significant shakeout in the industry as early as this winter. Some of those loss-making airlines that couldn’t make money when oil was at $40 a barrel certainly can’t survive this winter with oil at $80 a barrel.”

Carl Denton, managing director of Sven Carlson Aviation Consulting, says non-US airlines also have to deal with the strength of the US dollar when buying fuel, adding another cost dimension to the process.

“If you look at foreign exchange rates in 2014 relative to now, the US dollar is much stronger,” adds Denton. “We are in a situation at present where fuel price is increasing and foreign exchange rates for European carriers are also poor.”

Not everybody is particularly concerned about the recent fuel price rise. Willie Walsh, CEO of British Airways and Iberia owner IAG, says he is more worried about the disruptive impact of strikes by air traffic controllers in Europe this summer than a higher fuel bill.

“Some of the weak carriers are clearly looking even weaker with the fuel price where it is,” says Walsh. “I suspect the challenges they face are just going to increase. I wouldn’t be surprised to see a few of these weaker carriers slip further into difficulties and potentially see some exits from the markets in the later part of this year.”

Impact on routes

But what type of airlines and routes are most likely to be affected by the increase in fuel costs in the near future? Will the spectre of higher fuel costs force them to become more conservative in their choice of routes and even make them less patient in the time they are willing to give a route to become profitable?

Independent air transport consultant John Strickland, director of JLS Consulting, says: “It’s those airlines who have the least or no hedging and those whose overall non-fuel cost base is not sufficiently low who are the most vulnerable.

“They may not be able to absorb increases unless they have strong cash resources and may be forced to cut capacity or ultimately face outright failure.

“It certainly will make some routes more marginal or commercially unviable. Airlines will review frequencies, capacity, length of season or complete suspension of services.”

Although fuel accounts for a larger proportion of the overall cost of long-haul routes, Strickland adds: “The impact of higher costs will vary according to the mix of traffic and the amount of competition, regardless of whether routes are long-haul or short-haul.”

Denton adds that rising fuel bills mean that the longer the route, “the greater the risk and the larger the financial exposure can be”.

“Some long-haul destinations also have high fuel delivery costs which impact viability,” he adds. “If the market is strong and yields are high, then factors such as fuel are not a major issue. If, however, the route is weak, then such factors as fuel and foreign exchange will have a greater impact.”

As for opening up new routes, airlines may also become more cautious about their destination choice.

“Other factors such as the volume of aircraft deliveries can come into play, but with higher costs, carriers will be more risk averse,” says Denton. “New routes carry other costs such as marketing and building route awareness, linked with the greater unknown of a positive outcome.”

If all this sounds a little gloomy for route development, there are more positive signs away from the headline fuel price increase.

Despite downgrading its estimate for the profitability of the airline sector this year, IATA stresses that its current forecast still represents “solid profits” for the industry and not a return to the days when a fuel price spike meant aviation was “plunged back into losses”.

Even accounting for potentially higher airfares, passenger numbers are still expected to grow by 7% this year – well above the annual average of 5.5% seen over the past two decades.

European carriers reap rewards of fuel price hedging

European airlines are set to stave off the immediate impact of higher fuel prices after their hedging strategies paid off.

The region’s carriers are set to make a net profit of $8.6 billion in 2018 – up from $8.1 billion last year – as they secured more of their fuel through hedges, according to IATA’s financial forecast.

Conversely, North American airlines are set to suffer a year-on-year profit drop of $3.4 billion to $15 billion in 2018 as their lower rate of fuel hedging has made them “more immediately exposed” to the oil price rise.

But this competitive advantage for European carriers will dissipate over the few months if fuel prices remain high. Lower fuel prices were not enough to save three major carriers – Monarch, Air Berlin and Alitalia – from going into administration in 2017.

One European airline with a much lower level of fuel hedging is Norwegian (27% hedged for 2018), which has already been the subject of unsuccessful takeover bids from IAG. A continuation of higher fuel prices is likely to keep speculation bubbling about Norwegian’s future.